Overview

SuperEarn’s portfolio allocation turns a simple stablecoin deposit into stable, long-lasting yield. By diversifying across DeFi and RWA sectors, it reduces APY volatility and shields users from unexpected failures in any single protocol. Instead of chasing headline yields, SuperEarn allocates only to strategies that meet strict risk and liquidity criteria, using a liquidity- and risk-adjusted optimization framework to identify the most efficient opportunities. Through dynamic rebalancing across market cycles, users benefit from consistent and resilient performance.Key Principles

- We create the product we want to use and confidently deposit our own stablecoins into.

- SuperEarn do not invest in non-transparent protocols.

- Allocations are made only to underlying protocols that generate real yield. (e.g., Aave, Morpho).

- Even if the underlying protocol is reputable, we avoid curators that rely on collateral backed by opaque assets.

- SuperEarn avoid investing in vaults that generate yield through direct looping.

- All protocols that SuperEarn allocate capital are being done extensive risk due diligence using our risk framework to minimize risks.

Process

Risk Screening

See the risk framework pages for details on DeFi and RWA protocols.

Sector Diversification

Sector diversification is essential because it balances return and risk across fundamentally different yield sources. In the SuperEarn portfolio, DeFi and RWA sectors exhibit structurally low correlation – their performance drivers are almost independent. DeFi yields are influenced by market liquidity, on-chain activity, and funding rates, while RWA yields are anchored to real-world credit and treasury returns, which remain relatively stable even in downturns.

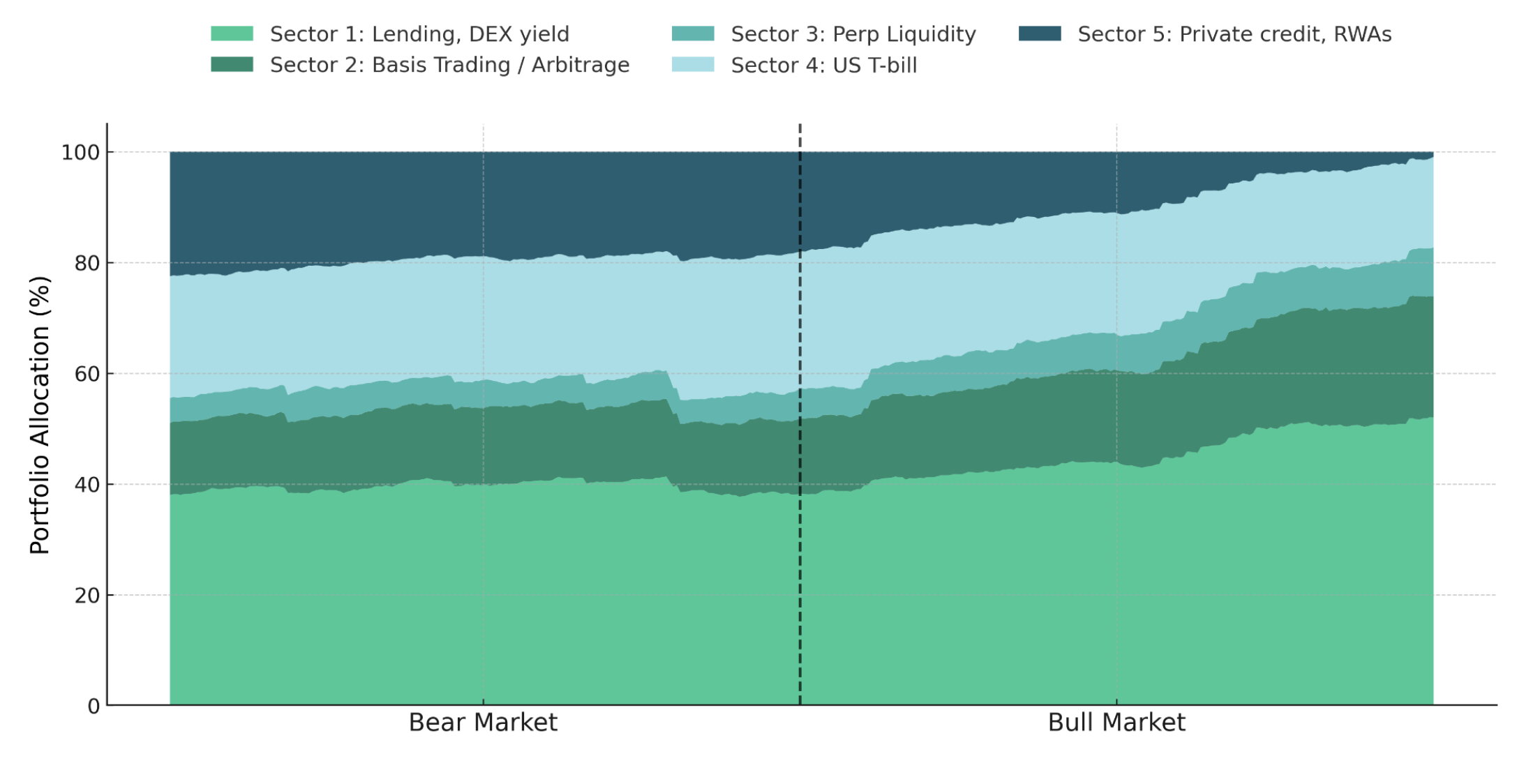

This low correlation enables counter-cyclical rebalancing: during bull markets, DeFi exposure can be increased to capture higher risk-adjusted returns, while in bear markets, RWA allocation is expanded to preserve stability and sustain baseline yield. Such diversification smooths portfolio volatility, enhances the liquidity-adjusted Sharpe ratio, and keeps performance more consistent across market regimes.

Liquidity- and Risk-Adjusted Optimization

This approach refines the traditional Sharpe ratio by incorporating liquidity and other risk costs. Instead of measuring excess return per unit of volatility alone, it penalizes assets with low liquidity, high trading costs, or elevated technical and collateral risks — allowing portfolio weights to favor the most resilient yield sources.

The result is a portfolio that balances return and risk while remaining robust under stressed or illiquid market conditions.

Example

Consider optimizing allocation between Morpho’s USDC/T lending vault and other yield sources. A standard Sharpe ratio might suggest that Morpho’s 8% APY with low volatility (around 0.5%) is the dominant choice, but this ignores liquidity and collateral considerations. Morpho positions can experience sustained utilization spikes, lower withdrawal liquidity, and exposure to higher-risk collateral types. Under SuperEarn’s optimization framework, the objective function includes explicit liquidity and risk cost terms.

This ensures capital flows toward the most liquidity- and risk-efficient yield opportunities, balancing return, volatility, and redemption feasibility.

Result: SuperEarn Portfolio

A sector-based, risk- and liquidity-adjusted portfolio that dynamically rebalances across bull and bear markets.